의사결정 나무 패키지

R에서는 의사결정 나무를 구현하기 위해서 다양한 패키지들을 제공합니다. 대표적으로는 rpart, tree, party가 있습니다.

이 패키지들의 차이점은 바로 "가치지기의 방법" 입니다.

- rpart: CART(classification and regression trees)을 사용합니다.

- tree: binary recursive partitioning을 사용합니다.

* 위 두개의 패키지들은 엔토로피와 지니계수를 사용해서 가치지기를 수행할 변수를 정합니다. 연산이 빠르다는 장점이 존재하지만 과적합될 가능성이 큽니다. 그래서 Pruning 과정을 통해서 과적합을 개선해 나가야 합니다.

- party: Unbiased recursive partitioning based on permutation test를 사용합니다. P-test를 거치게 된 중요도를 기준으로 가지치기 할 변수를 결정하기 때문에 별도의 가지치기 작업이 필요없습니다.

의사결정 나무 실습

1. 데이터 준비

credit<-read.csv("C:\\Users\\User\\Desktop\\머신러닝\\credit.csv")

head(credit)

checking_balance months_loan_duration credit_history purpose amount savings_balance

1 < 0 DM 6 critical furniture/appliances 1169 unknown

2 1 - 200 DM 48 good furniture/appliances 5951 < 100 DM

3 unknown 12 critical education 2096 < 100 DM

4 < 0 DM 42 good furniture/appliances 7882 < 100 DM

5 < 0 DM 24 poor car 4870 < 100 DM

6 unknown 36 good education 9055 unknown

employment_duration percent_of_income years_at_residence age other_credit housing

1 > 7 years 4 4 67 none own

2 1 - 4 years 2 2 22 none own

3 4 - 7 years 2 3 49 none own

4 4 - 7 years 2 4 45 none other

5 1 - 4 years 3 4 53 none other

6 1 - 4 years 2 4 35 none other

existing_loans_count job dependents phone default

1 2 skilled 1 yes no

2 1 skilled 1 no yes

3 1 unskilled 2 no no

4 1 skilled 2 no no

5 2 skilled 2 no yes

6 1 unskilled 2 yes nostr(credit)

summary(credit)'data.frame': 1000 obs. of 17 variables:

$ checking_balance : Factor w/ 4 levels "< 0 DM","> 200 DM",..: 1 3 4 1 1 4 4 3 4 3 ...

$ months_loan_duration: int 6 48 12 42 24 36 24 36 12 30 ...

$ credit_history : Factor w/ 5 levels "critical","good",..: 1 2 1 2 4 2 2 2 2 1 ...

$ purpose : Factor w/ 6 levels "business","car",..: 5 5 4 5 2 4 5 2 5 2 ...

$ amount : int 1169 5951 2096 7882 4870 9055 2835 6948 3059 5234 ...

$ savings_balance : Factor w/ 5 levels "< 100 DM","> 1000 DM",..: 5 1 1 1 1 5 4 1 2 1 ...

$ employment_duration : Factor w/ 5 levels "< 1 year","> 7 years",..: 2 3 4 4 3 3 2 3 4 5 ...

$ percent_of_income : int 4 2 2 2 3 2 3 2 2 4 ...

$ years_at_residence : int 4 2 3 4 4 4 4 2 4 2 ...

$ age : int 67 22 49 45 53 35 53 35 61 28 ...

$ other_credit : Factor w/ 3 levels "bank","none",..: 2 2 2 2 2 2 2 2 2 2 ...

$ housing : Factor w/ 3 levels "other","own",..: 2 2 2 1 1 1 2 3 2 2 ...

$ existing_loans_count: int 2 1 1 1 2 1 1 1 1 2 ...

$ job : Factor w/ 4 levels "management","skilled",..: 2 2 4 2 2 4 2 1 4 1 ...

$ dependents : int 1 1 2 2 2 2 1 1 1 1 ...

$ phone : Factor w/ 2 levels "no","yes": 2 1 1 1 1 2 1 2 1 1 ...

$ default : Factor w/ 2 levels "no","yes": 1 2 1 1 2 1 1 1 1 2 ... checking_balance months_loan_duration credit_history purpose amount

< 0 DM :274 Min. : 4.0 critical :293 business : 97 Min. : 250

> 200 DM : 63 1st Qu.:12.0 good :530 car :337 1st Qu.: 1366

1 - 200 DM:269 Median :18.0 perfect : 40 car0 : 12 Median : 2320

unknown :394 Mean :20.9 poor : 88 education : 59 Mean : 3271

3rd Qu.:24.0 very good: 49 furniture/appliances:473 3rd Qu.: 3972

Max. :72.0 renovations : 22 Max. :18424

savings_balance employment_duration percent_of_income years_at_residence age

< 100 DM :603 < 1 year :172 Min. :1.000 Min. :1.000 Min. :19.00

> 1000 DM : 48 > 7 years :253 1st Qu.:2.000 1st Qu.:2.000 1st Qu.:27.00

100 - 500 DM :103 1 - 4 years:339 Median :3.000 Median :3.000 Median :33.00

500 - 1000 DM: 63 4 - 7 years:174 Mean :2.973 Mean :2.845 Mean :35.55

unknown :183 unemployed : 62 3rd Qu.:4.000 3rd Qu.:4.000 3rd Qu.:42.00

Max. :4.000 Max. :4.000 Max. :75.00

other_credit housing existing_loans_count job dependents phone default

bank :139 other:108 Min. :1.000 management:148 Min. :1.000 no :596 no :700

none :814 own :713 1st Qu.:1.000 skilled :630 1st Qu.:1.000 yes:404 yes:300

store: 47 rent :179 Median :1.000 unemployed: 22 Median :1.000

Mean :1.407 unskilled :200 Mean :1.155

3rd Qu.:2.000 3rd Qu.:1.000

Max. :4.000 Max. :2.000

> table(credit$default) no yes

700 300 default는 채무불이행을 했는지에 대한 여부를 나타냅니다. 즉 우리가 예측해야 될 값을 의미합니다. table 함수를 써서 확인해봤을때 전체의 30%는 채무 불이행을 한 것을 확인하였습니다.

# 시드값을 설정하면서 동인한 난수열을 따르게 설정한다.

set.seed(1234)

train_sample<-sample(1000,700)

str(train_sample)학습데이터를 80% 테스트 데이터를 20%로 설정하였습니다.

train<-credit[train_sample,]

test<-credit[-train_sample,]

prop.table(table(train$default))

prop.table(table(test$default)) no yes

0.7014286 0.2985714 no yes

0.6966667 0.3033333 학습 데이터와 테스트 데이터를 완성 후 그 비율들을 비교해봤을때 비슷하게 할당이 된 것을 확인하였습니다.

2-1 모델 학습및 평가(rpart 패키지)

# rpart 패키지 사용

library(rpart)

tree_rp<- rpart(default~., data=train, method='class')

summary(tree_rp)Call:

rpart(formula = default ~ ., data = train, method = "class")

n= 700

CP nsplit rel error xerror xstd

1 0.08612440 0 1.0000000 1.0000000 0.05793201

2 0.03827751 3 0.7416268 0.7416268 0.05256163

3 0.02551834 4 0.7033493 0.7272727 0.05219354

4 0.01674641 7 0.6267943 0.7272727 0.05219354

5 0.01435407 9 0.5933014 0.7320574 0.05231715

6 0.01196172 13 0.5358852 0.7607656 0.05303980

7 0.01116427 15 0.5119617 0.7559809 0.05292159

8 0.01000000 18 0.4784689 0.7703349 0.05327360

다음은 생성된 나무를 시각화를 해보도록 하겠습니다. rpart에서는 rpart.plot 패키지를 사용해서 시각화를 진행할 수 있습니다.

library(rpart.plot)

install.packages("rpart.plot")

library(rpart.plot)

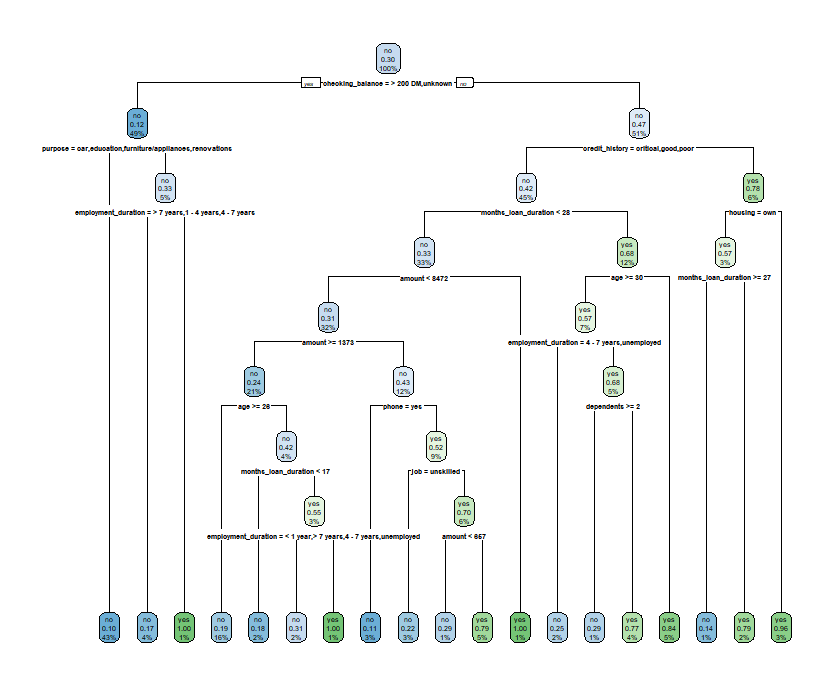

rpart.plot(tree_rp)

위에서 말했듯이 rpart 패키지는 과적합의 위험성이 크다고 하였습니다. 이 부분을 해결하기 위해서 가치지기를 수행 하도록 하겠습니다. 이때 사용되는 함수는 print.cp 함수입니다.

printcp(tree_rp)

Classification tree:

rpart(formula = default ~ ., data = train, method = "class")

Variables actually used in tree construction:

[1] age amount checking_balance credit_history

[5] dependents employment_duration housing job

[9] months_loan_duration phone purpose

Root node error: 209/700 = 0.29857

n= 700

CP nsplit rel error xerror xstd

1 0.086124 0 1.00000 1.00000 0.057932

2 0.038278 3 0.74163 0.74163 0.052562

3 0.025518 4 0.70335 0.72727 0.052194

4 0.016746 7 0.62679 0.72727 0.052194

5 0.014354 9 0.59330 0.73206 0.052317

6 0.011962 13 0.53589 0.76077 0.053040

7 0.011164 15 0.51196 0.75598 0.052922

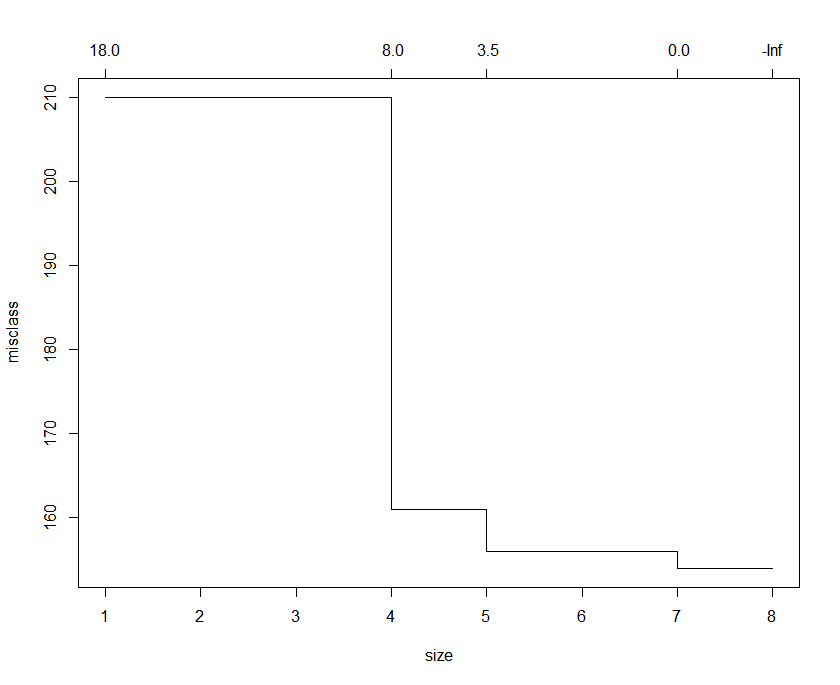

8 0.010000 18 0.47847 0.77033 0.053274plotcp(tree_rp)

xerror 값이 가장 낮은 split값을 선택하면 되는데요. 결과값과 그래프를 보면 7에서의 split에서 가장 낮은 값을 나타냅니다. split 7에서 cp값은 0.016746 이므로 대략 cp값을 0.02로 설정해 보겠습니다.

rpart_pr<-prune(tree_rp, cp=0.02)

rpartpred<-predict(rpart_pr, test, type='class')

confusionMatrix(rpartpred, test$default)Confusion Matrix and Statistics

Reference

Prediction no yes

no 169 57

yes 40 34

Accuracy : 0.6767

95% CI : (0.6205, 0.7293)

No Information Rate : 0.6967

P-Value [Acc > NIR] : 0.7936

Kappa : 0.1924

Mcnemar's Test P-Value : 0.1043

Sensitivity : 0.8086

Specificity : 0.3736

Pos Pred Value : 0.7478

Neg Pred Value : 0.4595

Prevalence : 0.6967

Detection Rate : 0.5633

Detection Prevalence : 0.7533

Balanced Accuracy : 0.5911

'Positive' Class : no

Confusion Matrix를 통해 성능 평가를 해본 결과 정확도는 약 0.67정도로 나타났습니다.

2-2 모델 학습및 평가(tree 패키지)

사용되는 패키지명은 tree 입니다.

install.packages("tree")

library(tree)

tree_tr<-tree(default~. , data=train)

summary(tree_tr)Classification tree:

tree(formula = default ~ ., data = train)

Variables actually used in tree construction:

[1] "checking_balance" "purpose" "employment_duration" "credit_history"

[5] "months_loan_duration" "amount" "housing"

Number of terminal nodes: 8

Residual mean deviance: 0.9198 = 636.5 / 692

Misclassification error rate: 0.2 = 140 / 700

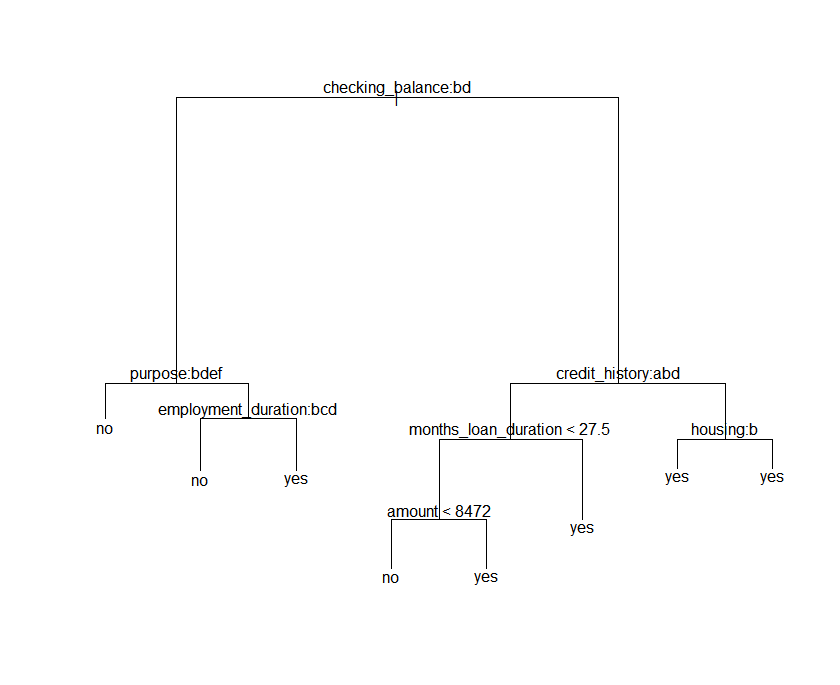

다음은 트리를 시각화를 해보겠습니다.

plot(tree_tr)

text(tree_tr)

트리는 이러한 구조를 가지고 있습니다. tree 패키지도 rapart와 동일하게 가지치기 과정이 필요합니다. 이때 사용되는 함수는 cv.tree함수를 사용해서 split개수를 정하도록 하겠습니다.

cv.tree<-cv.tree(tree_tr, FUN=prune.misclass)

분산값이 가장 작은 7로 split수를 지정하도록 하겠습니다.

prune_tree<-prune.misclass(tree_tr, best=7)

plot(prune_tree)

text(prune_tree)

트리를 시각화 해보니 이전보다 간단해진것을 알 수 있습니다.

Confusion Matrix and Statistics

Reference

Prediction no yes

no 180 66

yes 29 25

Accuracy : 0.6833

95% CI : (0.6274, 0.7356)

No Information Rate : 0.6967

P-Value [Acc > NIR] : 0.7158895

Kappa : 0.1536

Mcnemar's Test P-Value : 0.0002212

Sensitivity : 0.8612

Specificity : 0.2747

Pos Pred Value : 0.7317

Neg Pred Value : 0.4630

Prevalence : 0.6967

Detection Rate : 0.6000

Detection Prevalence : 0.8200

Balanced Accuracy : 0.5680

'Positive' Class : no 성능 평가를 해본 결과 정확도가 약 0.68로 rpart보다 약간 높은 예측률을 나타냈습니다.

2-3 모델 학습및 평가(party 패키지)

사용되는 패키지명은 party 입니다.

# party 패키지 사용

install.packages("party")

library(party)

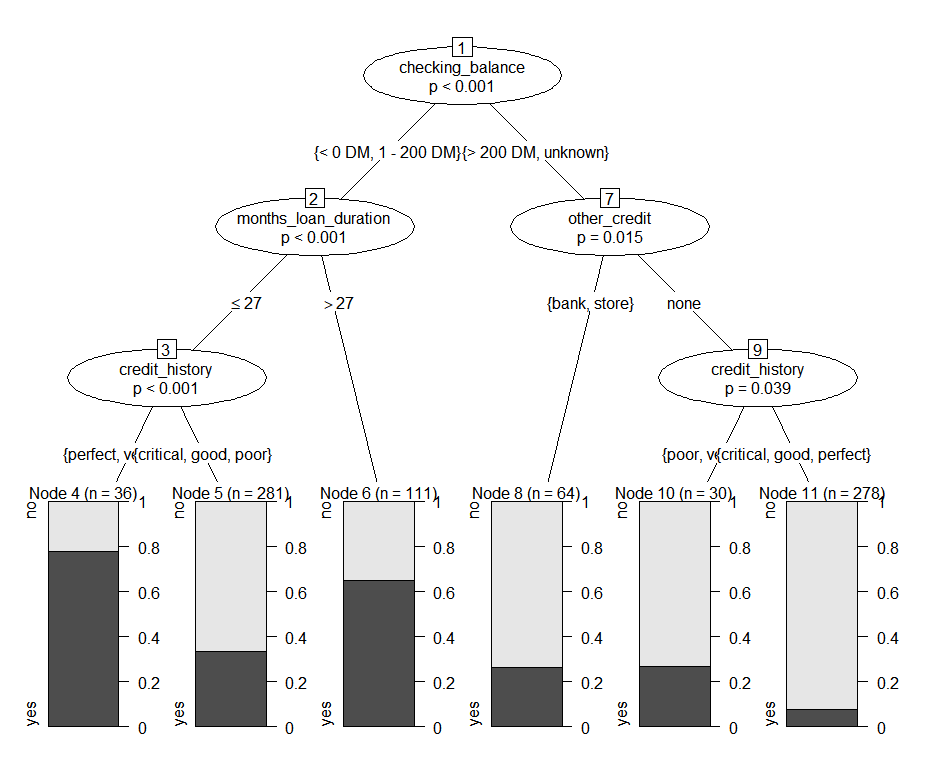

tree_pt<-ctree(default~., train)plot(tree_pt)

트리는 다음과 같이 생겼습니다. 앞의 예제들과는 약간 다른 시각화 모양이 나오는 것을 알 수 있습니다.

party패키지는 따로 가치치기 과정이 필요 없다고 앞에서 언급하였습니다. 따라서 바로 테스트를 하고 성능 평가를 진행 하도록 하겠습니다.

partypred<-predict(tree_pt, test)

confusionMatrix(partypred, test$default)

Confusion Matrix and Statistics

Reference

Prediction no yes

no 181 66

yes 28 25

Accuracy : 0.6867

95% CI : (0.6309, 0.7387)

No Information Rate : 0.6967

P-Value [Acc > NIR] : 0.6722447

Kappa : 0.1596

Mcnemar's Test P-Value : 0.0001355

Sensitivity : 0.8660

Specificity : 0.2747

Pos Pred Value : 0.7328

Neg Pred Value : 0.4717

Prevalence : 0.6967

Detection Rate : 0.6033

Detection Prevalence : 0.8233

Balanced Accuracy : 0.5704

'Positive' Class : no 성능 평가 결과 앞의 두 패키지들보다 정확도가 약간 높게 나왔습니다. 최종적으로는 party>tree>rpart순으로 성능이 좋게 나왔습니다.

하지만 모든 데이터에서 그러한 결과가 나오는 것은 아닙니다. 따라서 의사결정나무는 패키지 종류가 다양하기 때문에 데이터의 구조와 특징에 맞게 그 결과를 비교해서 가장 좋은 예측을 나타내는 패키지를 선택하는 것이 중요합니다.

'Machine Learning' 카테고리의 다른 글

| 회귀란? (0) | 2020.05.26 |

|---|---|

| ML 평가 지표 (0) | 2020.05.09 |

| K-NN 알고리즘 (0) | 2020.05.05 |

| 분류 실습(신용카드 사기 데이터) (0) | 2020.05.03 |

| LightGBM (3) | 2020.04.28 |